Cleaner, Smaller and Emptier: What Became of Latvia’s Banking Sector After Clean-Up

On our 15th anniversary, Re:Baltica revisits the issues it has long cared about. Then and now.

In the history of Latvian banking, February has often been a month of fateful turns.

These events amounted to an earthquake in Latvia’s banking sector.

“My last one-on-one conversation with [outgoing Prime Minister Māris] Kučinskis was that banking supervision somehow had to be fixed,” Kariņš told “I realised that either we radically changed the system or we would all sink together” Kariņš told Re:Baltica.

The reform launched seven years ago – cleansing banks of non-resident money, mostly originating in ex-USSR – effectively ended only this year. Moneyval, the Council of Europe’s anti-money laundering monitoring body, in February released Latvia’s latest evaluation. Their verdict: Latvia has built an effective, transparent system resilient to money-laundering risks.

“It is one of the best evaluations any country has received. Of roughly 40 recommendations, only one remains unmet, and it concerns specific professions such as notaries and real-estate agents,” Uldis Cērps, head of the Finance Latvia Association, told Re:Baltica.

Yet the overhaul also left behind a series of negatives. Governor of Latvian Central bank, Mārtiņš Kazāks, during a parliamentary committee hearing on this year’s priorities spelled out the wish list: more banks, more diverse services, greater competition, internationally competitive and export oriented sector.

What Remains?

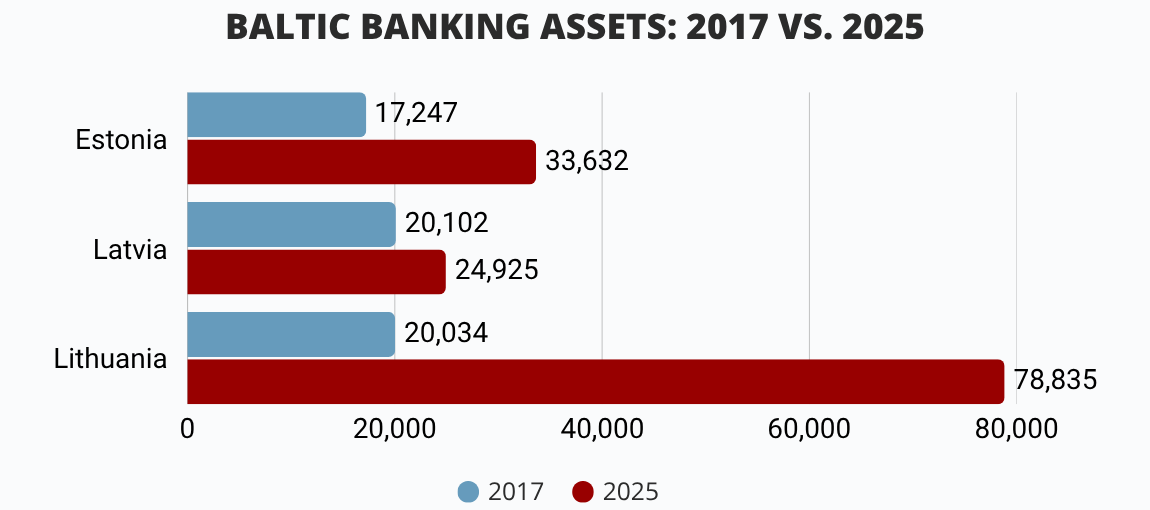

Before the overhaul, the bank markets of the three Baltic states were broadly similar in size.

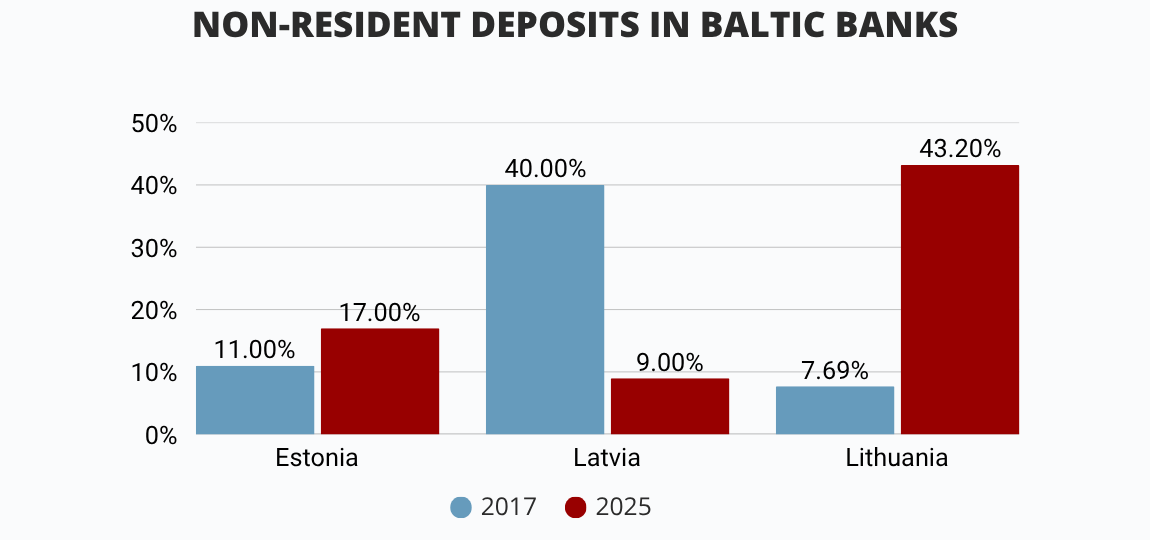

What set Latvia apart was the source of its money. Around 40 percent of deposits belonged to non-residents. This was the result of a policy dating back to the 1990s, when Latvia saw itself as a transit and financial bridge between East and West. The model was sustained both by lingering Communist Party-era connections among the new elite and by generous political donations from bankers.

Today, the sector is almost unrecognisable.

Before the clean-up, Latvia had 21 banks. Today, only 14 remain — including two newcomers, according to Bank of Latvia.

Non-residents now account for about 9 percent of deposits in Latvian banks, including both EU and non-EU clients. Meanwhile, foreign money in Lithuania has risen to a level even slightly above Latvia’s pre-overhaul share, largely thanks to Revolut, according to data from the Bank of Lithuania.

Among the major banks serving non-residents, only Rietumu Banka survived the overhaul. Its name, too, had regularly surfaced in money-laundering scandals. It escaped with a €20 million fine for money laundering in France — still neither collected nor paid — and several million euros in penalties in Latvia.

Among smaller institutions, only those that reinvented themselves survived.

One such example is Signet Bank. It began life in the 90s as the Latvian branch of Russia’s Bank Moskva under the name Latvijas Biznesa banka. Over time, it absorbed parts of other laundromats — Expobank and Latvijas Pasta banka. Later, the bank changed both its brand and ownership.

I met its CEO, Roberts Idelsons, at the bank’s headquarters in Riga’s art nouveau quarter. An installation by famous local graffiti artist, Kiwi, greets visitors in the lobby; contemporary art hangs on the walls. The atmosphere is that of an elite boutique bank — a place where, unless you have a million euros, there is little reason to walk in. Sunlight filters through stained-glass windows in the meeting room, while a modern painting of monkeys hangs on the opposite wall.

I first met Idelsons during the glory days of Parex Bank, which once advertised itself to clients as being closer than Switzerland. Idelsons was considered one of the industry’s rising stars and has witnessed every phase of Latvia’s “east-west bridge” period.

“I don’t like the word ‘survivors’, because we successfully transformed our business model and became a fairly respected institution,” he says (the bank expanded beyond investment baking into securities issuance and corporate lending). “Why couldn’t others do the same? Because their business was simply moving money from East to West. If that’s the only thing you know how to do, and one day someone tells you it’s over, you can’t build something new overnight.”

The demand for change came fast — within months.

In 2018, the head of Latvia’s financial regulator, Pēters Putniņš, summoned the executives of every non-resident bank and informed them that business could not continue as before. Like many banks serving non-residents, Signet held a licence allowing only 20 percent of its customers to be locals. Today its focus is domestic clients, and non-residents make up less than 10 percent of its customer base.

“Honestly, we were happy — genuinely happy,” Idelsons says when asked whether the overhaul was necessary. “It gave us the chance to build a normal bank. A normal business. To get rid of the stigma that if you owned a bank in Latvia, you were laundering money. I’d been waiting for the moment when all that would finally become history, because it was obvious that sooner or later it would end. What I didn’t expect was that it would happen in this form.”

Within five years, he says, that message had filtered through every level of international business. “That is a very, very important positive outcome.”

The result is a Latvian banking sector that is clean, but substantially smaller than those of its neighbours. The three Baltic states started from roughly the same position. Today, Lithuania’s banking sector is more than three times larger.

That reflects not only the consequences of the overhaul and the Revolut effect, but Latvia’s broader economic underperformance.

According to Cērps, no comprehensive economic assessment of the overhaul has ever been carried out. The only estimate available remains a 2014 KPMG study, which put the contribution of non-resident banking to the economy at 1.14 percent of GDP.

But, he argues, that is not the most important consideration.

The economy has become more transparent. The rule of law has strengthened. The influence of organised crime has diminished. Geopolitical risks have been reduced. “The fact that Latvia’s financial system was free of Russian money when the full-scale invasion began was geopolitically extremely important,” Cērps says.

Here Comes The Scandinavians

During those years, banks in Latvia were also fined one after another. Yet only the former owners and executives of ABLV have ended up in the dock.

The trials continue. No one can predict when they will end.

Former Financial Intelligence Unit (FIU) chief Ilze Znotiņa describes the proceedings as extraordinary. “This is a unique case. There are very few examples in the world where people at the very highest level are sitting in the defendants’ dock,” she said. “Objectively, the prosecution and police might not have had the resources to investigate something this complex. It is a remarkable act of state determination to pursue this case and try to secure convictions.”

Will they succeed?

“I don’t know,” she says. “Our Economic Affairs Court is still very inexperienced.”

The creation of that court became one of the structural reforms born of the overhaul. Others were trusting regulation and oversight to the central bank and giving adequate resources to FIU.

We met in café on the left bank of the Daugava River, where she gave her first interview after taking office years earlier. Znotiņa is wearing a camouflage hoodie emblazoned with the word Countryside. These days, she says, she is preoccupied with how to protect civilian infrastructure in wartime.

“I’m conflicted myself,” she says. “How do you balance that overwhelming desire to be clean and white against the fact that investment is still needed? And I’ve been spoiled by hearing everyone say: look at Lithuania, they got everything.”

Looking back now, she says there were things that could have been handled more subtly. “But not the idea that we had a choice. If it had been left to us, we would have done nothing.”

She describes Latvia’s earlier fight against money laundering as a form of ‘deliberate incompetence’, placing much of the blame on the regulator’s leadership at the time, which she says effectively sabotaged the process.

Its chairman, Pēters Putniņš, paid for the overhaul with his position – though he departed with a golden parachute.

Putniņš argues that his conflict with the others, including PM, stemmed from a fundamentally different vision of how the clean-up should be executed. He preferred a gradual approach which would allow to preserve viable business.

“The process was politically unmanaged and excessively open to outside opinions that were neither filtered nor critically assessed,” he says.

Putniņš recalls nights sitting alone in his office. “There were times when I sat there at midnight, phone on the desk, thinking I should call someone higher up. Then I realised there was no point because I wouldn’t get any answer. They would simply say: decide for yourself.”

We met at the Re:Baltica office. Compared with our last conversation, during the liquidation of ABLV, this one is calm. “I fought for clear rules. If there are five requirements, then there should be five. Not five to ten, and if you get it wrong someone comes along and fines you.”

Today, virtually everyone involved in the overhaul agrees on one thing: banks went too far in their customer checks.

What is striking is that no one is willing to accept responsibility for it.

Now, years later, Kazāks puts it this way: “We hear banks say that regulation does not allow something, but in most cases that simply is not true. If there are risks, manage them, but don’t beat everyone with the same stick.”

Over time, requirements have been simplified. Central bank is proposing to lawmakers scrapping Latvia’s additional national rules altogether and relying solely on EU, which will come into force in 2027.

Ironically, the excesses of the overhaul eventually caught up even with the man who launched it.

I meet Krišjānis Kariņš online. He is now in Brussels, where he works as an adviser for the Swedish public-affairs firm KREAB.

He recalls what happened when his first salary arrived. “I signed a contract with them. The first payment comes in through Swedbank. The bank sends me a letter packed with legal provisions, as if I were a criminal, strongly suggesting that my account could be frozen until I explain this and that,” said ex-PM whose work history and current employment can be verified with a few clicks online. “The banks are frightened, and so are their owners.”

For Kariņš, the deeper problem lies elsewhere. “At the root of it is the culture of punishment we learn from school onwards. We don’t look at the substance of things. We just punish.”

The Scandinavians Stayed, But…

The overhaul also revealed that it was not only local banks that had been laundering dirty money through the Baltics. Attracted by the profits, Scandinavian banks were eager to have a piece.

The scandal became so large that Sweden’s banks at one point considered leaving the region altogether. Kariņš says he travelled to Sweden to meet executives from SEB and Swedbank and urge them to remain in the Baltics. “They told me that the fall in their share price resulting from the scandals was larger than anything they could earn back in the Baltics over many years,” he says

Kariņš appealed to them on broader grounds. “I argued on a human level that it was important for us – for the Latvian government – that they stay. But it was obvious that management in Latvia had received instructions from shareholders: don’t create any more problems.”

The Scandinavians stayed. Today the sector is dominated by the Big Four: Swedbank, SEB, Luminor and Citadele.

Together they control more than four-fifths of the market.

The Competition Council is currently examining the sector and has promised conclusions by the end of June.

The data suggest that Latvia’s largest banks weathered the overhaul remarkably well. The sector’s profits declined for only two years. Just one year after the most intense phase of the clean-up, profits had already exceeded pre-overhaul levels.

They fell again only in 2025, after the introduction of a windfall-profit tax and changes of EURIBOR.

The cost of compliance was largely borne by ordinary Latvians.

Banks invested heavily in customer-screening systems and hired additional compliance staff — in some large institutions, several hundred employees Consumers ultimately paid for those investments through higher fees and more expensive services.

Former regulator Pēters Putniņš believes the system was originally designed for monitoring non-residents, not ordinary Latvian customers.

“The system we live under today was built for non-residents. Local residents should not have had to suffer the way they do now, and banks would not normally have had to bear such costs,” says former regulator Putniņš. “I told the prime minister at the time: don’t impose on local residents the same template you imposed on non-residents. You’ll kill the whole thing.”

Central Bank acknowledges that the cost of financial services remains a problem. Speaking about lending rates, Kazāks told MPs: “Our goal is to bring prices closer to the European level, not the Baltic level.”

The legacy of the overhaul arrives regularly by email in the form of court rulings.

Higher courts have repeatedly overturned decisions of the Economic Affairs Court and ordered millions of euros belonging to ABLV clients to be confiscated and transferred to the state.

The hearings are held behind closed doors.

As a result, the public cannot see the full picture of the people who used Latvia’s banking system to launder stolen wealth.

The cases range from individuals connected to Tajikistan’s railway leadership to associates of former Ukrainian President Viktor Yanukovych, who fled to Russia.

According to Re:Baltica’s calculations, courts have already recognised at least €31.1 million as criminal proceeds this year alone.

Yet even as Latvia celebrates its success, some of the people most closely associated with the overhaul worry that victory could breed complacency. Znotiņa fears that Latvia has a habit of falling into the same trap every decade, getting into a hole, collapsing and then reinventing itself. “Do you think the dirty boys and girls weren’t waiting for this assessment? Of course they were,” she says.

The sources of dirty money may change, she says, but the money itself does not: “There won’t be dirty money from Russia anymore, but even before that we saw flows coming through Ukraine, Moldova and Central Asian countries. Or Emirates. Look at the beautiful Waterfront project we are going to have, right?”

Despite all their disagreements, everyone interviewed for this story agrees on one point: the overhaul was necessary.

Even those who criticise how it was carried out do not argue that it should never have happened.

The dispute is over the price.

“That assessment is fantastic. We were effectively in the grey zone, and now we are out. After Russia’s war in Ukraine, there should no longer be any questions about whether it was necessary or not,” says Kariņš.

Cērps agrees: “The capital overhaul was unquestionably necessary. Let me repeat – if only for the simple reason that our financial system should not pose a threat to national security after Russia’s full-scale invasion of Ukraine.”

Even Putniņš agrees that, if the excesses applied to local residents are adjusted, the reform may ultimately turn out to have been worthwhile:

“That story is not over. We need another ten years. Then we’ll see, because we need to see where our neighbours end up and whether there is still something that can be improved here.”

Asked why Latvia has failed to attract significant new banking players, Roberts Idelsons offers a blunt answer: “Why not? The answer is very simple. It’s a very small market, and for major players it simply isn’t interesting.”

Then he pauses. “And judging by our previous experience, perhaps it isn’t such a terrible thing that it isn’t.”

Meanwhile, the government has approved a strategy to increase the number of fintech companies by one third and turn Latvia into a competitive European hub for them.

“We have seen growing interest in Latvia and hope that it will continue. But we also see that banks evaluate cooperation from a purely business perspective, and there are only so many people here,” Cērps sums up the outcome of the overhaul. “We are no longer a regional financial centre. We are the local Latvian market.”

Author: Sanita Jemberga

Editor: Nellija Ločmele (IR)

Illustrations: Emīls Miko Rode

Graphics and Technical Support: Madara Indāne

Social Media: Inese Braže, Ieva Strazdiņa

Translated with AI assistance

![]()

INDEPENDENT JOURNALISM NEEDS INDEPENDENT FINANCING If you like our work, support us! LV38RIKO0001060112712